Credit: Apple

Credit: Apple

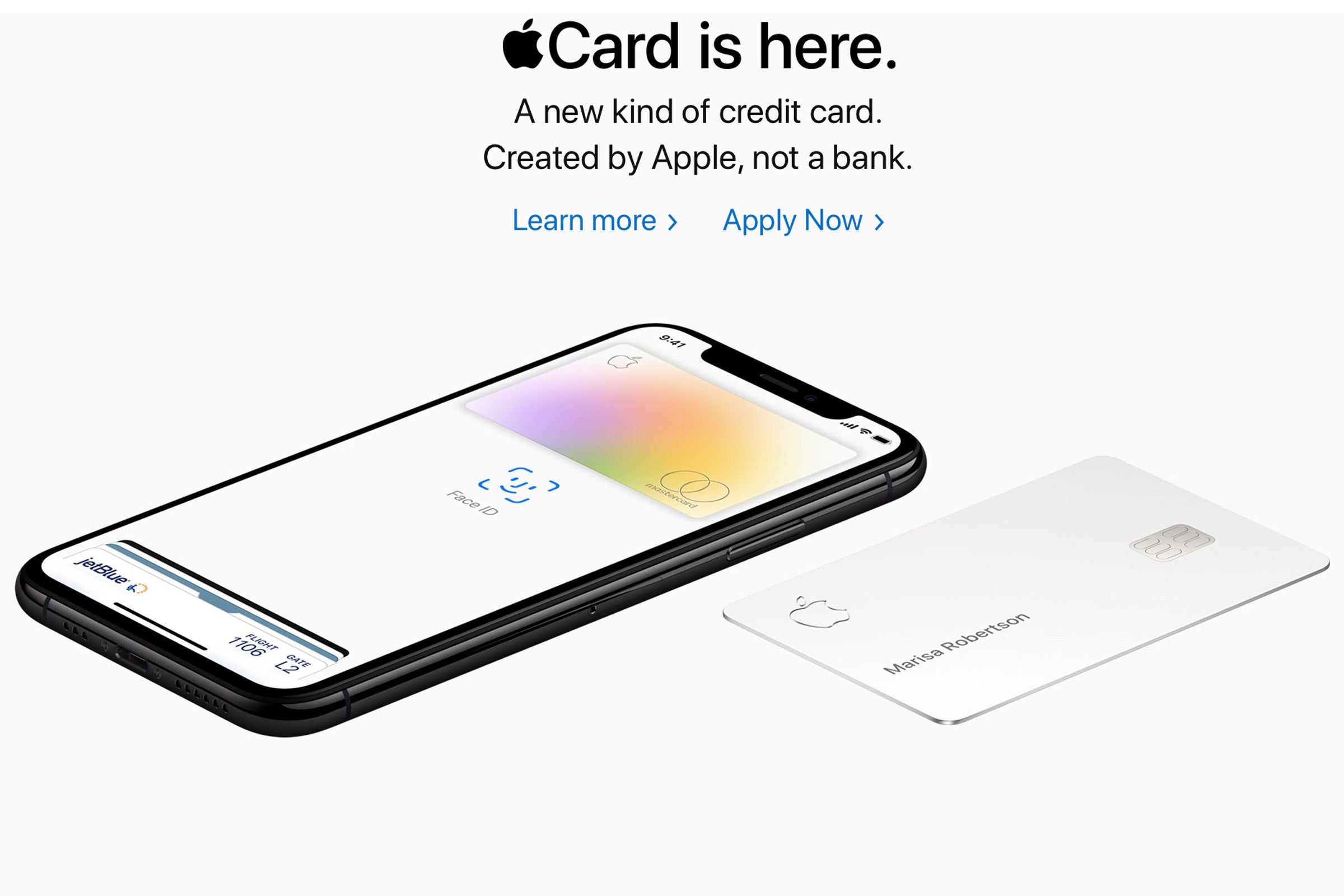

If you navigate over to Apple.com today, you’ll see a brand new product at the top of the homepage. Like so many iPhones, iPads, and Macs that have come before, the beautiful images and enticing tagline make you want to get one immediately, complete with a button to do so.

Except, the newest Apple thing doesn’t have a screen. It’s not a shiny thing you can buy on a payment plan or lust over at the Apple Store. In fact, it actually won’t cost you anything to get it. At least not up front. No, for this product all you have to turn over is your credit. You know, the thing that needs to be in good standing to get a house or a car or, just an iPhone XS under Apple’s Upgrade Program. And it’s not just about buying stuff. Your credit score and history could also be determining factors when renting an apartment, signing up for cable television, even being considered for a job.

Apple

Apple

The Apple Card is being positioned like it's a new phone—but it's a far more dangerous purchase.

But you might not realize that when you click to sign up for the Apple Card. Other than being at least 18 years old, the only requirements for ownership are an iPhone and an Apple ID associated with an iCloud account that is in good standing with Apple. If you have those two things, it will only take a few seconds to get a line of credit hooked up directly to your iPhone. That could be a dangerous thing in the wrong hands.

It’s the ultimate lock-in, with the laser‑etched titanium card as the ultimate Apple status symbol. With millions of people signing up just to put the titanium card in their wallet, Apple will surely be handing out credit to people that shouldn't have it. If you’re not careful or responsible with it, it could end up costing you way more than a broken iPhone XS screen.

Debt as a service

Like any credit card looking for your application, the Apple Card is full of promises—low interest rates, no fees, cash-back rewards—as well as exclusive benefits for purchases made through Apple. Except the usual credit-card lingo doesn’t apply. You won’t see anything about APR or find any fine print on the offer page, and it’s all presented like the next big thing you need to have: A new kind of credit card. Created by Apple, not a bank.

While the Apple Card might be filled with the delightful little details that we’ve come to expect from Apple—beautiful spending trackers, an animated digital card that reflects light as if you were holding it, privacy and security at the forefront—at its core, Apple Card is still a credit card backed by a bank that will charge you interest if you don’t pay on time.

Apple

Apple

The Apple Card might have an Apple logo on the front, but inside its a MasterCard issued by Goldman Sachs.

I’m not saying that Apple is trying to hide the fact that it’s loaning you money to buy stuff. But whether or not it “encourages you to pay less interest” or “makes it easy to spot trends in your spending, so you can decide if you want to change them,” Apple’s positioning of Apple Card as the next must-have accessory for your iPhone is dangerous for people who don’t understand how carrying balances and missing payments can affect them. Even if you never buy anything with it, the Apple Card will still have an impact on your credit score.

The usual credit card risks are compounded when you factor in the Apple appeal. Apple is selling its usual "it just works" factor with the Apple Card, but its greatest strength could also be a detriment. Not only is the Apple Card designed to be solely tied to your iPhone, Apple and Goldman Sachs have also made it difficult to pay your bill without an iOS device. With Apple Card, Apple is potentially locking in the entire stack—device, payment, subscription, and debt—for every Apple product you buy. Basically, if you take out an Apple Card and carry a balance, you’re tied to your iPhone until you pay it off.

Is that Apple’s intention with Apple Card? Likely not. But it’s hard to look at the Apple Card marketing and not see how people could fall into a huge trap just to get their hands on one of those shiny new titanium cards. Credit cards are supposed to be things you get out of necessity, not desire. By positioning it as a cool new gadget, Apple is turning debt into a thing people crave.

Titanium risk

For responsible buyers, Apple Card could very well be the game-changer Apple claims it is. Daily rewards, location-based charges, visual spending trackers, and clear interest rates and charges are a very Apple way to disrupt the financial services market with transparency and innovation, and the iPhone’s Wallet app is a tremendous delivery system. But you need to be mature and responsible enough to use them.

Apple

Apple

The Apple Card's spending trackers are fantastic—if you're responsible enough to use them.

No matter how much smarter it is than the other MasterCards in your wallet, the Apple Card can be a dangerous tool for debt. But while other companies position their card as an option at checkout to pay for the thing you just bought—as Apple did with the Barclaycard Visa with Apple Rewards it offered previously—Apple is selling the Apple Card as an impulse buy, even a status symbol.

That’s not the same as a new gadget that you may or may not need. With Apple Card, Apple may be selling you something that could end up costing you way more than an iPhone—or a Mac Pro for that matter.